The Ultimate Guide to Spousal Social Security Eligibility

Why Spousal Social Security Eligibility Could Be Worth Thousands of Dollars to You

Understanding spousal social security eligibility is one of the most important steps a married, divorced, or widowed person can take before claiming retirement benefits.

Quick answer: Who qualifies for spousal Social Security benefits?

| Who | Key Requirements |

|---|---|

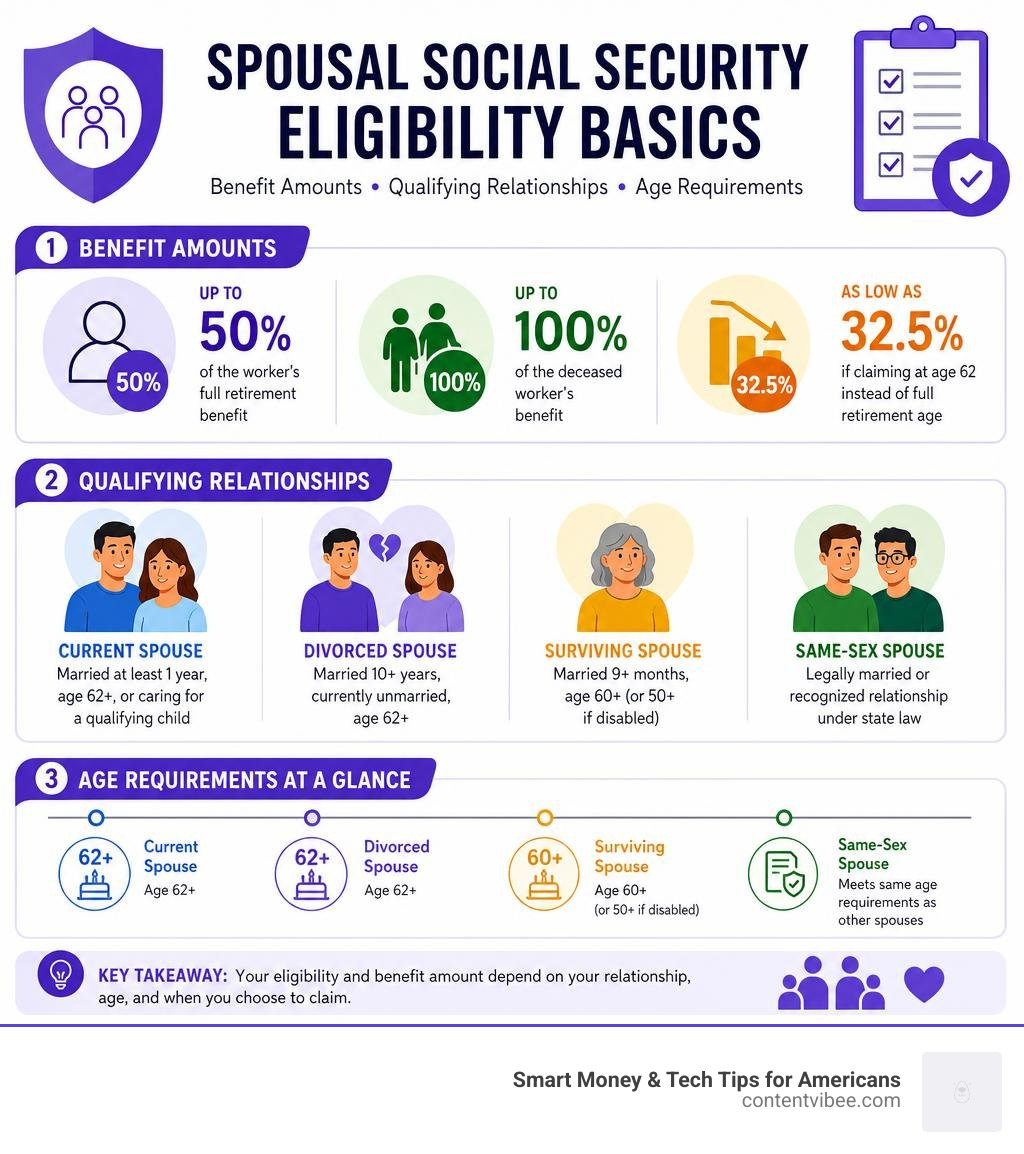

| Current spouse | Married at least 1 year, age 62+, or caring for a qualifying child |

| Divorced spouse | Married 10+ years, currently unmarried, age 62+ |

| Surviving spouse | Married 9+ months, age 60+ (or 50+ if disabled) |

| Same-sex spouse | Legally married or recognized relationship under state law |

A few numbers that show why this matters:

- 97% of people age 60 to 89 receive or will receive Social Security

- A spouse can receive up to 50% of the worker’s full retirement benefit

- A surviving spouse can receive up to 100% of the deceased worker’s benefit

- Claiming at age 62 instead of full retirement age can cut that benefit down to as little as 32.5%

These numbers add up to real money over a lifetime. Yet many couples leave significant benefits unclaimed simply because the rules are confusing.

The rules cover current spouses, divorced spouses, same-sex couples, surviving spouses, and even spouses who never worked a day in their lives. Each group has its own set of age requirements, marriage duration rules, and benefit calculations.

This guide breaks all of it down in plain language so you can make confident, informed decisions.

Who Qualifies for Spousal Social Security Eligibility?

To understand spousal social security eligibility, we first need to look at how the Social Security Administration (SSA) defines a “spouse.” While it might sound straightforward, the SSA actually recognizes several different types of marital relationships to ensure families are protected.

According to the official SSA – POMS: RS 00202.001 – Definitions and Requirements for Spouse Benefits, a claimant can qualify as a spouse if they are legally married to the worker under the laws of the state where the worker lives.

However, the law also covers “deemed spouses.” A deemed spouse is someone who entered into a marriage ceremony in good faith, believing it was legally valid, only to find out later that a legal impediment (such as an incomplete prior divorce) made the marriage technically invalid. The SSA recognizes these good-faith unions so that innocent spouses are not cut off from the benefits they deserve.

Requirements for Current Spouses

For a current, legally married spouse to qualify for benefits on a partner’s record, there are three primary pathways. Under SSA Handbook § 305, you must meet at least one of the following conditions:

- The One-Year Marriage Rule: You must have been legally married to the worker for at least one continuous year immediately before filing your application.

- The Natural Parent Exception: If you and your spouse are the natural parents of a child together, the one-year duration requirement is waived.

- Prior Entitlement: If you were already entitled (or potentially entitled) to certain Social Security auxiliary benefits—such as widow’s, parent’s, or disabled adult child’s benefits—in the month before you married your current spouse, you do not have to wait a year to qualify.

Additionally, the primary worker must already be receiving their own retirement or disability benefits for you to claim a spousal benefit on their record.

Same-Sex Couples and Spousal Social Security Eligibility

Same-sex couples enjoy the exact same rights and access to spousal benefits as opposite-sex couples. Following the landmark Supreme Court decisions in Windsor and Obergefell, the SSA recognizes same-sex marriages for all retirement, disability, and survivor benefits.

According to SSA – POMS: GN 00210.100 – Same-Sex Relationships, the SSA determines eligibility based on whether the marriage was legally recognized in the state where it was performed or where the worker lived.

Crucially, the SSA calculates the duration of the marriage from the actual date of the marriage or the establishment of a recognized Non-Marital Legal Relationship (NMLR), such as a civil union or registered domestic partnership. They do not calculate it from the dates of the Supreme Court rulings. This means same-sex couples who have been married for decades can easily satisfy the one-year or ten-year duration requirements.

Divorced Spouses and Deemed Spouses

If you are divorced, you might still have a claim on your ex-spouse’s earnings record. To qualify as a divorced spouse, your marriage must have lasted for at least 10 consecutive years before the divorce became final.

If you meet this 10-year milestone and are currently unmarried, you can claim benefits based on your ex-spouse’s record once both of you are at least 62 years old. The best part? Your ex-spouse does not even need to have filed for their own retirement benefits yet, as long as you have been divorced for at least two consecutive years and they are eligible to claim.

Age, Marriage Duration, and Child-in-Care Rules

Timing is everything when it comes to Social Security. To map out your strategy, you must understand the rules regarding age, marriage duration, and the “child-in-care” exceptions.

The 10-Year Rule for Divorced Spouses

For divorced individuals, the 10-year marriage rule is non-negotiable. If your marriage lasted 9 years and 364 days, the SSA cannot grant you divorced spousal benefits.

As outlined in SSA – POMS: NL 00711.025 – Wife’s Benefits Paragraphs, a divorced spouse must also remain unmarried to collect on an ex-partner’s record. If you remarry, your eligibility on your ex-spouse’s record terminates (unless your new marriage ends by death, divorce, or annulment).

Furthermore, if your ex-spouse has not yet filed for their own benefits, you must wait until the divorce has been finalized for at least two continuous years before you can file for divorced spousal benefits on their record.

Child-in-Care Exceptions to Age Requirements

While 62 is generally the minimum age to claim spousal benefits, there is a major exception: the child-in-care provision.

If you are caring for a child who is under the age of 16, or a child of any age who became disabled before age 22, you can claim spousal benefits at any age. Under this exception:

- Your spousal benefits are not reduced for early claiming, even if you are under your Full Retirement Age (FRA).

- The child must be entitled to child’s benefits on your spouse’s Social Security record.

- Once the youngest non-disabled child turns 16, your child-in-care spousal benefits will stop unless you elect to receive reduced benefits (if you are at least 62) or if you are caring for a disabled adult child.

How Spousal Benefits Are Calculated

Your spousal benefit is based on your partner’s Primary Insurance Amount (PIA). The PIA is the monthly amount your spouse is entitled to receive at their Full Retirement Age.

The maximum spousal benefit you can receive is 50% of your spouse’s PIA. However, this maximum is only available if you wait until your own Full Retirement Age to claim.

Impact of Early Claiming on Spousal Social Security Eligibility

If you decide to claim your spousal benefit before reaching your Full Retirement Age, the SSA will permanently reduce your monthly payment. The reduction is calculated using a strict formula:

- First 36 months early: Reduced by 25/36 of 1% for each month.

- Any additional months early (up to 24 more months): Reduced by 5/12 of 1% for each month.

If your Full Retirement Age is 67 (which is the case for everyone born in 1960 or later) and you claim your spousal benefit at age 62 (60 months early), your benefit will be reduced by a total of 35%. This means instead of getting 50% of your spouse’s PIA, you will receive just 32.5%.

| Claiming Age | Months Before FRA (Assuming FRA of 67) | Spousal Benefit Percentage (of Spouse’s PIA) |

|---|---|---|

| 67 (FRA) | 0 | 50.0% |

| 66 | 12 | 45.8% |

| 65 | 24 | 41.7% |

| 64 | 36 | 37.5% |

| 63 | 48 | 35.0% |

| 62 | 60 | 32.5% |

Dual Entitlement: Your Own Benefit vs. Spousal Benefit

Many people wonder, “Can I collect my own retirement benefit and my spousal benefit at the same time?”

The short answer is no. The SSA does not allow “double-dipping.” This is governed by the dual entitlement rule.

When you apply for benefits, the SSA will calculate both your own retirement benefit (based on your work history) and your spousal benefit. If your own retirement benefit is higher than the spousal benefit, you will receive your own benefit. If the spousal benefit is higher, the SSA will pay your retirement benefit first, and then add an auxiliary spousal benefit to make up the difference. You receive an amount equal to the larger of the two benefits.

Survivor Benefits for Widows, Widowers, and Divorced Survivors

Losing a partner is a difficult life event. Fortunately, Social Security survivor benefits are designed to provide financial stability during this time.

Unlike living spousal benefits (which max out at 50%), a surviving spouse can receive up to 100% of the deceased worker’s benefit, including any delayed retirement credits the worker earned.

According to SSA – POMS: RS 00207.001 – Widow(er)’s Benefits Definitions and Requirements, the basic requirements for a surviving spouse include:

- Marriage Duration: You must have been married to the deceased worker for at least 9 months immediately before their death (exceptions apply for accidental deaths or military service).

- Age: You can claim survivor benefits as early as age 60 (or age 50 if you are disabled).

- Divorced Survivors: If you are a surviving divorced spouse, you can claim survivor benefits if your marriage lasted at least 10 years and you are currently unmarried (or remarried after age 60).

Disability Provisions for Surviving Spouses

If you are a widow, widower, or surviving divorced spouse who becomes disabled, you do not have to wait until age 60 to claim survivor benefits.

Under Title II disability provisions, disabled survivors can claim benefits as early as age 50, provided their disability began within seven years of the worker’s death or within seven years of the last month they received mother’s or father’s benefits.

That a standard 5-month waiting period applies to disabled widow(er) benefits before payments can begin.

Modern Claiming Strategies and Recent Rule Changes

In the past, couples used advanced claiming strategies like “file-and-suspend” or filing a “restricted application.” These strategies allowed one spouse to claim a spousal benefit while letting their own retirement benefit grow by 8% per year through delayed retirement credits.

However, the Bipartisan Budget Act of 2015 phased out these loopholes:

- File-and-Suspend: This strategy is completely gone. If a worker suspends their own retirement benefit, all auxiliary benefits on their record (including spousal benefits) are also suspended.

- Restricted Applications: This option was limited to individuals born before January 2, 1954.

Because we are now in June 2026, anyone born before 1954 is already at least 72 years old. Consequently, the restricted application strategy has officially phased out for new retirees. Today, when you file for retirement or spousal benefits, you are subject to deemed filing. This means filing for one benefit automatically serves as filing for the other, and the SSA will automatically award you the higher of the two amounts.

How to Apply and Required Documentation

Ready to file? You can submit your application for retirement and spousal benefits online, by phone, or in person at your local SSA office.

Note: Survivor benefits cannot be applied for online. You must call the SSA or visit a local office to apply for survivor benefits.

Required Evidence and Forms for Claiming

To ensure a smooth application process, you must gather your documentation ahead of time. The SSA has strict evidence standards outlined in SSA – POMS: RS 00202.050 – Spouse’s Benefits – Evidence and Forms Requirements.

Be prepared to provide:

- Your birth certificate or other proof of age (always required if you are 62 or older).

- Proof of marriage (such as a marriage certificate) to establish your relationship.

- A divorce decree if you are claiming as a divorced spouse.

- Proof of U.S. citizenship or lawful alien status.

- Your spouse’s Social Security number and date of birth.

- Your bank routing and account numbers for direct deposit.

Frequently Asked Questions about Spousal Benefits

Can I receive both my own retirement benefit and a spousal benefit?

No. Under the dual entitlement rule, you cannot receive both benefits in full. The SSA will pay your own retirement benefit first. If your spousal benefit is higher, they will add an extra amount to your check so that your total payment matches the higher spousal benefit rate.

Does my ex-spouse’s claiming affect my own spousal benefit?

No. If you qualify for divorced spousal benefits, your claim is entirely independent. Your ex-spouse will not be notified, their own benefit amount will not be reduced, and any benefits paid to their current spouse will not be affected.

What is the maximum spousal benefit I can receive?

The maximum spousal benefit is 50% of your spouse’s Primary Insurance Amount (PIA) at their Full Retirement Age. Earning delayed retirement credits (by waiting past age 67 to claim) will increase your spouse’s personal benefit, but it will not increase your spousal benefit.

Conclusion

Navigating spousal social security eligibility can feel overwhelming, but taking the time to understand the rules can secure thousands of dollars in extra retirement income for your household. Whether you are married, divorced, or widowed, knowing your options is the key to a secure financial future.

At Smart Money & Tech Tips for Americans, we are dedicated to helping you make smart financial choices. Take control of your retirement planning today!