The No-Nonsense Guide to Fidelity Robo Advisor Fees

What You’re Actually Paying for Fidelity’s Robo Advisor

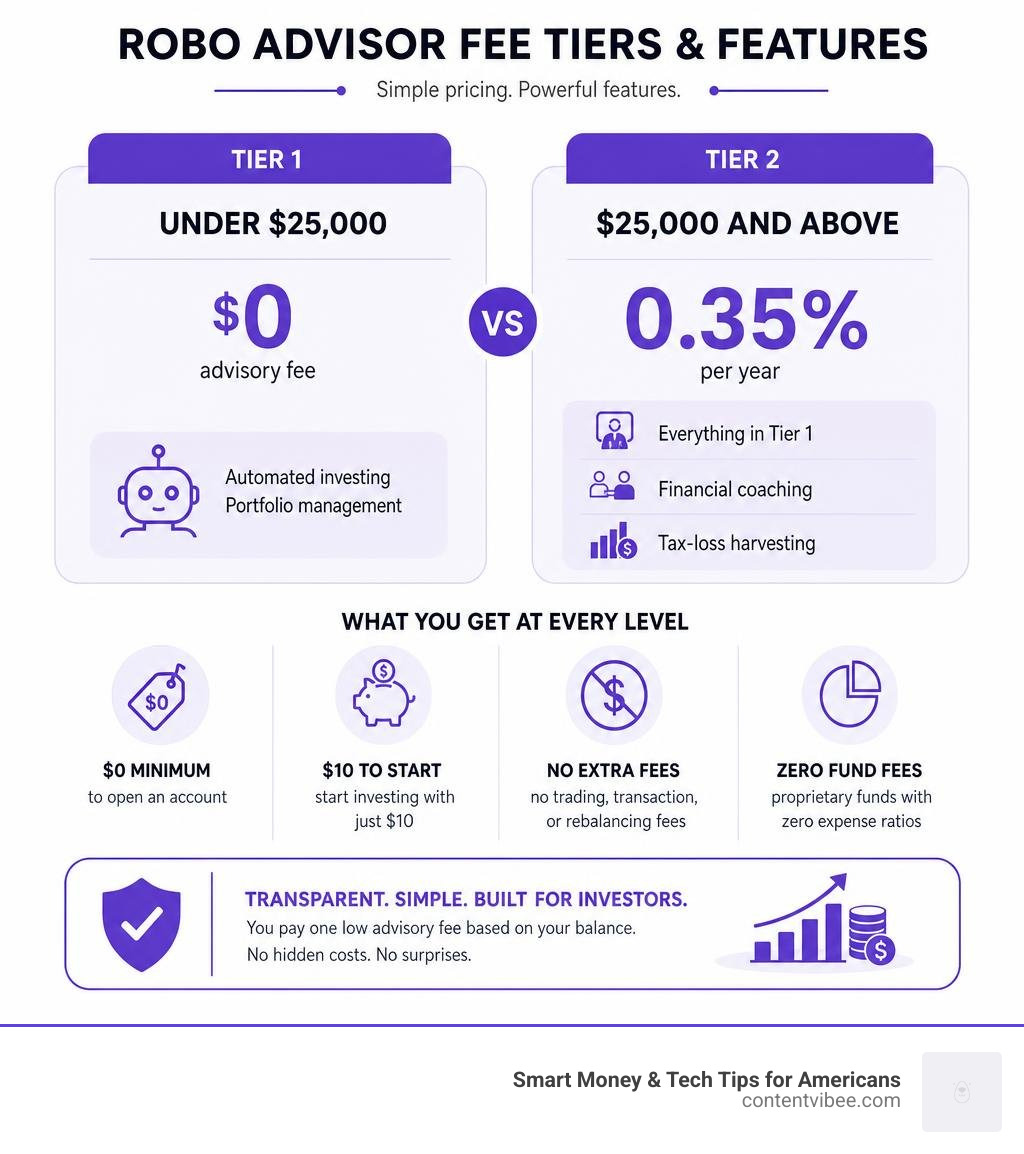

Fidelity robo advisor fees are among the most straightforward in the industry — and for many investors, the cost is literally zero.

Here’s the quick answer:

| Account Balance | Advisory Fee | What’s Included |

|---|---|---|

| Under $25,000 | $0 | Automated investing, portfolio management |

| $25,000 and above | 0.35% per year | Everything above + financial coaching + tax-loss harvesting |

A few other fast facts:

- $0 minimum to open a Fidelity Go account

- $10 is all you need to start investing

- No trading fees, transaction fees, or rebalancing fees at any balance level

- Fidelity Go uses proprietary Flex funds with zero expense ratios, meaning no hidden fund costs on top of the advisory fee

So the total cost for most new investors? Nothing. And even at the paid tier, 0.35% per year on a $25,000 balance works out to about $87.50 a year.

But fees alone don’t tell the whole story. Fidelity also offers higher-tier managed services — like Wealth Management and Private Wealth Management — with very different fee structures. And if you’re comparing Fidelity Go to competitors like Schwab or Vanguard, there are a few important differences worth knowing.

This guide breaks all of it down, clearly and without the jargon.

A Complete Breakdown of Fidelity Robo Advisor Fees

When we talk about automated investing, we often expect a maze of fine print. Fortunately, Fidelity’s pricing model for its robo-advisory service, Fidelity Go, is incredibly clean. By aligning its pricing with your account balance, the platform makes it easy to know exactly what you are paying and when.

To explore their complete pricing philosophy, you can read more about their Straightforward and Transparent Pricing – Fidelity Investments. Let’s dig into how these tiers work in practice.

No-Fee Tier for Balances Under $25,000

If you are just starting out, building an emergency fund, or testing the waters of automated investing, we have great news: Fidelity Go charges absolutely nothing for accounts with balances under $25,000.

There is no catch here. You get a professionally designed, diversified portfolio that is automatically monitored and rebalanced by human specialists and algorithms alike. You do not have to worry about monthly maintenance fees, annual account fees, or hidden transaction costs.

This $0 tier makes the Fidelity Go | Invest With Our Robo Advisor program one of the absolute best entry-level options for hands-off investors. It allows your money to grow completely unburdened by management fees during those crucial early stages of wealth building.

The 0.35% Tier for Larger Balances

Once your account balance reaches $25,000, Fidelity Go transitions you into its paid tier. At this point, you will pay an annual advisory fee of 0.35% of your assets under management.

How does this math work in the real world?

- On a $25,000 balance, you will pay $87.50 per year (about $7.29 a month).

- On a $50,000 balance, you will pay $175 per year (about $14.58 a month).

- On a $100,000 balance, you will pay $350 per year (about $29.17 a month).

While some investors might feel a bit disappointed to leave the free tier behind, the 0.35% fee unlocks two highly valuable features that can easily pay for themselves:

- Unlimited 1-on-1 Financial Coaching: You get access to live, 30-minute phone consultations with human financial professionals. Whether you want to talk about buying a home, planning for retirement, or budgeting, you can schedule these calls whenever you need guidance.

- Tax-Loss Harvesting: For taxable (non-retirement) accounts, the robo-advisor will automatically look for opportunities to sell investments that have dipped in value. This offsets your capital gains and can reduce your overall tax bill at the end of the year.

Comparing Fidelity Go and Hybrid Advisory Services

As your net worth grows, your financial needs often become more complex. While a basic robo-advisor is excellent for building a nest egg, you might eventually crave a more customized, human-led approach. Fidelity offers several levels of wealth management, but the leap in fees can be significant.

How Fidelity Robo Advisor Fees Compare to Wealth Management

To put the Fidelity robo advisor fees of 0.35% into perspective, it helps to look at the broader menu of Fidelity’s advisory programs.

- Fidelity Go (Robo-Advisor): Charges 0% under $25,000, and 0.35% for balances over $25,000. It is primarily digital, with coaching calls added at the higher tier.

- Fidelity Wealth Management: This service is designed for larger portfolios and carries an annual advisory fee ranging from 0.50% to 1.50%. It provides you with a dedicated financial advisor, comprehensive estate planning, and more advanced portfolio customization.

- Fidelity Private Wealth Management: Geared toward ultra-high-net-worth individuals, this tier offers bespoke estate, tax, and investment strategies. The advisory fees range from 0.20% to 1.04%, but it requires a massive capital commitment (typically millions of dollars).

If you are looking for simple, automated growth, jumping to full Wealth Management might mean paying three to four times more in annual fees. For most everyday investors, the robo-advisor remains the most cost-effective path.

How Fidelity Robo Advisor Fees Compare to Hybrid Services

Fidelity also offers a middle-ground option known as Fidelity Personalized Planning & Advice. This is a hybrid robo-advisor that bridges the gap between pure digital automation and full-scale wealth management. You can learn more about this option directly from the Make real progress on your financial goals page.

Here is how the hybrid service compares to the standard robo-advisor:

- Fee Structure: The hybrid service charges a flat 0.50% annual advisory fee, regardless of your balance.

- Minimum Investment: It requires a $25,000 minimum to get started.

- What You Get: It combines the digital portfolio management of a robo-advisor with more structured, goal-based planning tools and direct, ongoing access to coaching.

If you have exactly $25,000, the hybrid service will cost you roughly $125 a year, whereas the standard Fidelity Go robo-advisor would cost you $87.50. The difference is relatively small, but as your balance climbs to $100,000 or more, that 0.15% gap in fees becomes more noticeable.

Hidden Costs: Expense Ratios and Transaction Fees

When comparing robo-advisors, looking only at the “advisory fee” is a common trap. Many platforms place your money into third-party Exchange-Traded Funds (ETFs) or mutual funds. These underlying funds charge their own internal management fees, known as expense ratios.

If a robo-advisor charges a 0.25% advisory fee but builds your portfolio with funds that charge an average 0.15% expense ratio, your actual total cost is 0.40% per year.

Fidelity side-steps this issue entirely using a highly unique strategy.

Proprietary Flex Funds with Zero Expense Ratios

To keep your total costs as low as possible, Fidelity Go builds your portfolio using proprietary Fidelity Flex mutual funds.

These Flex funds are specifically designed for fee-based and managed accounts. They carry a 0% expense ratio. That means you do not pay a single penny in fund management fees.

Because of this setup, the advisory fee you pay to Fidelity Go is truly “all-inclusive.” If you are on the free tier (under $25,000), your total investment cost is absolutely zero. If you are on the paid tier ($25,000+), your total cost is capped strictly at 0.35%. This level of pricing transparency is incredibly rare in the financial services world.

Trading and Rebalancing Costs

Another area where investors often get nickel-and-dimed is transaction fees. Fortunately, we found no such hidden traps here.

According to the Fidelity Go | Robo Advisor FAQs, your advisory fee covers all administrative and trading costs. There are:

- $0 transaction fees

- $0 rebalancing fees

- $0 account maintenance fees

Whether the market is volatile and requires frequent portfolio rebalancing, or you are making weekly deposits into your account, you will never see a trade commission or transaction fee on your statement.

Frequently Asked Questions About Fidelity Go

Navigating automated investing can bring up plenty of practical questions. We have compiled the most common inquiries to help you master your understanding of how this service operates.

What is the minimum balance required to start investing?

You do not need a fortune to start building your wealth. There is a $0 minimum to open a Fidelity Go account.

Once your account is open, you only need to deposit $10 to kick off the automated investing process. The algorithms and portfolio managers will take that $10 and spread it across a diversified mix of zero-expense-ratio Flex funds aligned with your personal risk tolerance.

Are tax-loss harvesting and coaching included in the fees?

Yes, but only if you qualify for the paid tier.

Tax-loss harvesting and unlimited 1-on-1 financial coaching calls are unlocked automatically once your account balance reaches $25,000. These services are fully covered by your 0.35% annual advisory fee. There are no extra charges or subscription fees to speak with a coach or utilize the tax-optimization tools.

If your balance is under $25,000, you will not have access to these two features, but you also won’t pay any advisory fees.

Can I use Fidelity Go for retirement accounts like IRAs?

Absolutely. Fidelity Go is highly flexible when it comes to the types of accounts you can open. You can set up a managed retirement account by visiting the Managed Retirement Account | A New Way to IRA | Fidelity Investments page.

Supported accounts include:

- Traditional IRAs

- Roth IRAs

- Rollover IRAs

- SEP IRAs

- Health Savings Accounts (HSAs)

- Standard Taxable Accounts (Individual or Joint)

As we navigate through 2026, keep in mind the current contribution limits to maximize your tax advantages:

- IRA Contribution Limits (2026): $7,500 annually (plus an additional $1,100 catch-up contribution if you are age 50 or older).

- HSA Contribution Limits (2026): $4,400 for individual coverage and $8,750 for family coverage.

Using a robo-advisor for an HSA is an excellent way to grow your medical nest egg completely hands-off, while your retirement accounts benefit from automated, disciplined rebalancing over the long haul.

Conclusion

At Smart Money & Tech Tips for Americans, we believe that understanding where your money goes is the first step toward true financial freedom. High fees can quietly erode your investment returns over time, making fee transparency one of the most critical factors when choosing a platform.

Fidelity Go stands out as an incredibly competitive option. With its $0 fee tier for balances under $25,000, zero-expense-ratio Flex funds, and a straightforward 0.35% fee for larger accounts, it offers a highly accessible path to professional wealth management.

To see how these costs stack up against the broader market and to ensure you are making the smartest choice for your wallet, it is always wise to compare multiple platforms and analyze their complete fee structures. Taking a few minutes to review your options today can save you thousands of dollars in fees tomorrow. Happy investing!