The Ultimate Checklist for Your Application for Spousal Benefits

What You Need to Know Before Filing an Application for Spousal Benefits

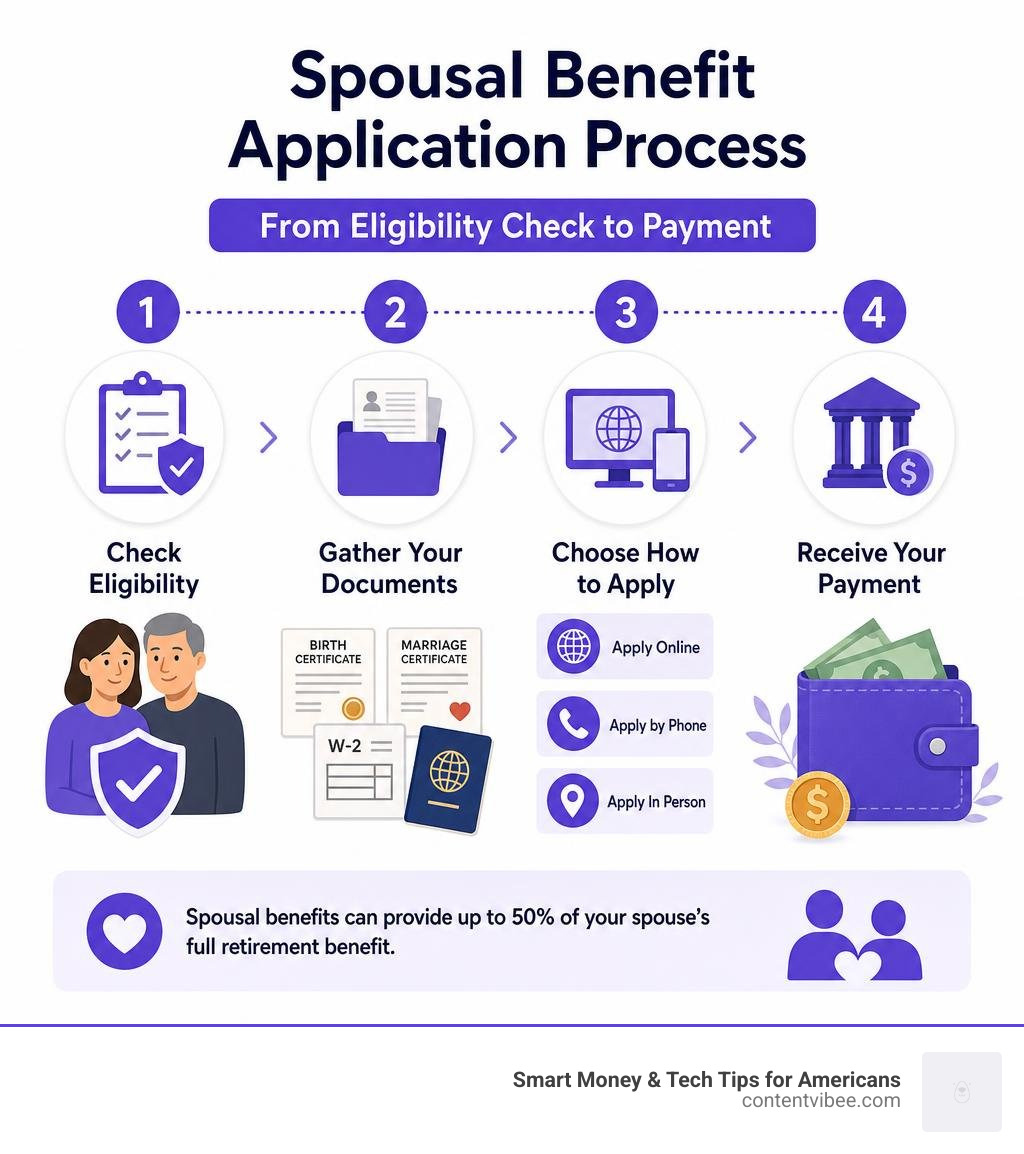

Want a quick answer? Here’s how to apply for spousal benefits in 4 steps:

- Check eligibility — You must be at least 62 (or any age if caring for a qualifying child under 16), married for at least one year, and your spouse must already be collecting Social Security retirement or disability benefits.

- Gather your documents — Birth certificate, marriage certificate (or divorce decree), W-2 forms, and proof of citizenship if needed.

- Choose how to apply — Online at ssa.gov (if you’re within 3 months of age 62 or older), by phone at 1-800-772-1213, or in person at your local Social Security office.

- Know your benefit range — You can receive between 32.5% and 50% of your spouse’s full retirement benefit, depending on when you claim.

Millions of Americans leave money on the table simply because they don’t know how spousal Social Security benefits work — or they wait too long to apply.

If your own work history is limited, or your personal Social Security benefit is small, a spousal benefit could significantly boost your retirement income. It can be worth up to 50% of your spouse’s full retirement benefit — without reducing what your spouse receives.

The rules aren’t always obvious. The timing of when you apply matters a lot. Claiming at 62 instead of waiting until your full retirement age can permanently reduce your benefit. And divorced spouses have their own separate set of rules to follow.

This checklist walks you through everything — eligibility, calculations, required documents, and exactly how to submit your application — so you don’t miss a step or make a costly mistake.

Eligibility Requirements for Spousal and Divorced Spouse Benefits

Navigating the Social Security Administration (SSA) maze can feel like reading a foreign language. However, the foundational eligibility rules for spousal benefits are relatively straightforward once you break them down.

To qualify for a spousal benefit, you must generally be married to someone who is already receiving Social Security retirement or disability benefits. Additionally, you must meet the age threshold of 62, unless you are caring for a qualifying child. Under the SSA rules, a qualifying child is defined as a child of the primary worker who is under the age of 16 or who became disabled before age 22.

The SSA has strict guidelines regarding who qualifies as a spouse. These include legal spouses, deemed spouses (marriages entered into in good faith that may have a technical legal impediment), and common-law spouses depending on the state of residence. You can review the exact definitions in the SSA definitions and requirements manual.

Requirements for Current Spouses

For current spouses, the most critical rule is the marriage duration. You must have been continuously married to the primary worker for at least one full year immediately before filing your application for spousal benefits.

There are a few rare exceptions to the one-year rule. For example, if you are the parent of your spouse’s biological child, or if you were eligible for certain other Social Security benefits (like survivor or disability benefits) in the month before you married, you might not have to wait a full year.

Additionally, your spouse must be actively entitled to either Retirement Insurance Benefits (RIB) or Disability Insurance Benefits (DIB). If your spouse has not yet claimed their own benefit, you cannot claim a spousal benefit based on their record.

Requirements for Divorced Spouses

If you are divorced, you may still be eligible to claim benefits based on your ex-spouse’s earnings record. The SSA has specific protections in place to ensure that divorced individuals are not left without financial security in retirement.

To qualify as a divorced spouse, you must meet the following criteria:

- The 10-Year Rule: Your marriage to your ex-spouse must have lasted for at least 10 continuous years before the divorce was finalized.

- The 2-Year Divorce Rule: If your ex-spouse has not yet applied for their own retirement benefits, but is eligible to receive them, you can still apply on their record independently—provided you have been divorced for at least two continuous years.

- Marital Status: You must currently be unmarried. If you remarry, you generally lose eligibility for benefits on your ex-spouse’s record (unless your subsequent marriage ends by death, divorce, or annulment).

- Age Requirement: You must be at least 62 years old.

The beauty of independent entitlement is that your ex-spouse does not need to be retired or collecting benefits for you to claim, as long as they are eligible and you meet the two-year divorce waiting period.

How to Calculate Your Spousal Benefit and the Cost of Claiming Early

The maximum spousal benefit you can receive is 50% of your spouse’s Primary Insurance Amount (PIA). The PIA is the amount your spouse is entitled to receive at their Full Retirement Age (FRA).

It is a common misconception that if your spouse claims their retirement benefit early (which reduces their monthly payout), your spousal benefit is also reduced. This is incorrect! Your spousal benefit is always calculated based on their PIA (their benefit at full retirement age), not their actual reduced benefit.

However, when you file your own application for spousal benefits is the single most important factor in determining your actual monthly check. If you claim before reaching your own full retirement age, your benefit will be permanently reduced.

| Your Claiming Age | Spousal Benefit Percentage (FRA 66) | Spousal Benefit Percentage (FRA 67) |

|---|---|---|

| 67 (Full Retirement Age) | 50.0% | 50.0% |

| 66 | 50.0% | 45.8% |

| 65 | 45.8% | 41.7% |

| 64 | 41.7% | 37.5% |

| 63 | 37.5% | 35.0% |

| 62 | 35.0% | 32.5% |

The Impact of Claiming at Age 62

Claiming your spousal benefit as early as possible—at age 62—comes with a steep financial penalty. If your full retirement age is 67 (which is the case for anyone born in 1960 or later), claiming at 62 permanently reduces your spousal benefit to just 32.5% of your partner’s PIA. If your full retirement age is 66, the benefit at age 62 is reduced to 35%.

This is a lifetime reduction. Once you file early, your monthly check is locked in at that lower rate (aside from annual Cost-of-Living Adjustments, or COLA). If you do not need the income immediately, waiting even a year or two can noticeably increase your monthly retirement cash flow.

Maximizing Your Monthly Payout

To get the absolute maximum spousal benefit, you must wait until you reach your own Full Retirement Age.

Unlike personal retirement benefits, spousal benefits do not earn delayed retirement credits. While your personal retirement benefit increases by 8% for every year you delay claiming past your FRA (up to age 70), a spousal benefit tops out at your FRA. There is absolutely no financial benefit to waiting past your FRA to file an application for spousal benefits.

If you are the lower earner, a smart coordination strategy is to have the higher-earning spouse delay claiming their own benefit as long as possible (up to age 70) to maximize their monthly check, while you claim your spousal benefit immediately upon reaching your own FRA.

Step-by-Step Guide to Your Application for Spousal Benefits

Ready to file? You have three ways to submit your application for spousal benefits:

- Online: This is the fastest and most convenient method. You can apply online at ssa.gov if you are within three months of turning 62 or older.

- By Phone: You can call the SSA’s national toll-free service at 1-800-772-1213 (TTY 1-800-325-0778) to schedule an appointment or complete the application over the phone.

- In Person: You can visit your local Social Security office. We highly recommend scheduling an appointment in advance to avoid spending hours in the waiting room.

Before you begin, it is helpful to look over the official Form SSA-2 instructions to understand the exact structure of the questions the SSA will ask.

Gathering Your Required Documentation

To ensure a smooth application process, you should gather all necessary documents beforehand. The SSA requires original documents or certified copies from the issuing agency—they will not accept standard photocopies of certificates.

Here is your document checklist:

- Proof of Age: Your original birth certificate.

- Proof of Citizenship: A U.S. passport or naturalization certificate if you were born outside the United States.

- Marriage Certificate: The original civil marriage certificate to prove your relationship.

- Divorce Decree: If you are applying as a divorced spouse, you must provide your final divorce decree.

- W-2 Forms or Tax Returns: Your W-2 forms or self-employment tax returns for the prior year (photocopies are acceptable for tax documents).

- Military Discharge Papers: If you had military service prior to 1968, you may need to provide your Form DD-214.

For a comprehensive breakdown of evidentiary rules and acceptable alternatives if you are missing a document, refer to the SSA evidence and forms requirements manual. Do not delay filing your application if you are missing some documents; the SSA can often help you obtain them!

Submitting the Application (Form SSA-2-BK)

When you are ready to apply, you will fill out Form SSA-2-BK (either online or with an agent). The SSA estimates that it takes about 11 minutes to read the instructions, gather your facts, and complete the form.

During the application process, you will be asked whether you wish to enroll in Medicare Part B. If you are close to age 65, this is an important decision, as delaying enrollment can lead to a permanent 10% premium penalty for every 12-month period you were eligible but not enrolled.

You will also need to provide your bank routing and account numbers to set up direct deposit. The federal government requires all benefit payments to be delivered electronically.

A note for educators and public employees: If you are a member of a state public pension program, such as California’s CalSTRS, your benefits may be divided differently under community property laws. If you are a nonmember spouse looking to claim a portion of a public pension, you will need to complete specific state forms, such as the CalSTRS nonmember spouse application, which is entirely separate from the federal Social Security process.

Key Differences: Current Spouses vs. Divorced Spouses

While the financial calculation for spousal benefits is largely the same for current and divorced spouses, the administrative rules differ significantly.

One of the biggest concerns divorced individuals have is whether their application will cause friction with their ex-spouse. We want to reassure you: your ex-spouse is never notified by the SSA when you file on their record. The application is kept entirely confidential to protect your privacy.

Furthermore, claiming benefits as a divorced spouse has absolutely zero impact on the benefit amount your ex-spouse (or their current spouse) receives. Even if a worker has multiple ex-spouses who all qualify for benefits on their record, every single one of them can collect their full 50% spousal benefit without reducing anyone else’s check.

| Feature | Current Spouse | Divorced Spouse |

|---|---|---|

| Marriage Duration Requirement | Minimum 1 year | Minimum 10 years |

| Worker Must Be Collecting? | Yes | No (if divorced 2+ years) |

| Ex-Spouse Notified? | N/A | No |

| Impact on Other Spouses’ Benefits | None | None |

| Remarriage Rules | Must remain married | Must remain unmarried |

Understanding Recent Policy Changes and Survivor Benefits

If you are researching Social Security strategies, you might run into outdated articles discussing complex maneuvers like “file-and-suspend” or “restricted applications.”

These strategies were largely eliminated by the Bipartisan Budget Act of 2015. Under current rules, “deemed filing” applies to almost everyone. This means when you apply for retirement benefits, the SSA automatically files you for both your personal benefit and your spousal benefit, and pays you the higher of the two.

The option to file a restricted application—where you claim only a spousal benefit at FRA while allowing your own personal benefit to grow until age 70—is now only available to individuals born before January 2, 1954. If you were born after that date, you can no longer use this strategy.

How Survivor Benefits Differ

It is vital to distinguish spousal benefits from survivor benefits, as they operate under completely different rules:

- Benefit Amount: While a spousal benefit maxes out at 50% of the worker’s PIA, a surviving spouse can receive up to 100% of the deceased spouse’s actual benefit.

- Age Threshold: Surviving spouses can begin collecting survivor benefits as early as age 60 (or age 50 if disabled), whereas spousal benefits require you to be 62.

- Caring for Children: If you are caring for the deceased worker’s child who is under 16 or disabled, you can receive survivor benefits at any age.

- Remarriage: If a surviving spouse remarries after age 60, they do not lose their eligibility for survivor benefits on their deceased spouse’s record.

For those who have lived or worked abroad, some international pension plans have similar structures. For example, if you have ties to Finland, you can look into the international spouse’s pension options through Kela to see how foreign survivor benefits are processed.

Frequently Asked Questions About Spousal Benefits

What Documents Do I Need for an Application for Spousal Benefits?

You will need to provide original documents (not photocopies) to the SSA, including your birth certificate, proof of U.S. citizenship or lawful alien status, your marriage certificate, and your W-2 forms or self-employment tax returns from the previous year. If you are divorced, you must provide your final divorce decree. If you served in the military before 1968, you should also have your military discharge papers handy.

Can I Complete an Application for Spousal Benefits Online?

Yes! You can complete your application online at ssa.gov if you are at least 61 years and 9 months old (within 3 months of eligibility) and want your benefits to start within the next 4 months. If the online portal does not show the spousal option clearly, you can complete the initial application and schedule a follow-up phone appointment with an SSA representative to ensure your spousal claim is properly attached to your partner’s record.

Can I Receive Both My Own Benefit and a Spousal Benefit?

No, the SSA does not allow “double dipping.” Under the deemed filing rules, when you apply, the SSA will calculate both your personal retirement benefit and your spousal benefit. If your personal benefit is higher, you will receive that amount. If the spousal benefit is higher, you will receive your personal benefit first, plus an additional spousal top-off to bring your total monthly payment up to the spousal benefit amount.

Conclusion

At Smart Money & Tech Tips for Americans, we believe that securing your financial future shouldn’t require a degree in bureaucracy. Filing your application for spousal benefits is a highly effective way to maximize your household’s retirement income, but timing is everything.

By understanding the rules, gathering your original civil documents early, and waiting until your Full Retirement Age if your budget allows, you can avoid permanent benefit reductions and steer clear of common claiming pitfalls.

For more tips on navigating your retirement options and making the most of your hard-earned government benefits, explore our comprehensive personal finance guides and resources.