How Much Does Health Insurance Actually Cost in California?

What Are Covered CA Rates Right Now?

Covered CA rates for 2026 have a preliminary weighted average increase of 10.3% — well below the national average of 20%. But what you actually pay depends on several personal factors.

Here’s a quick snapshot of key 2026 rate facts:

| Factor | Key Detail |

|---|---|

| Statewide average rate increase | 10.3% |

| National average rate increase | ~20% |

| If you shop and switch to lowest-cost plan | ~1.0% average change |

| State subsidies for low-income enrollees | $190 million allocated |

| Enrollees at risk from expired federal credits | 1.7 million Californians |

| Benchmark Silver plan (40-year-old, Sacramento) | $638/month before subsidies |

The big story in 2026 isn’t just the rate increase — it’s what happened to federal help. Enhanced federal premium tax credits expired on December 31, 2025. For many Californians, that means paying significantly more out of pocket, even if the base rate increase looks modest on paper.

Nearly 1.9 million Californians are enrolled in Covered California plans as of early 2025 — a record high. That means more people than ever are affected by these changes.

California has stepped in with $190 million in state subsidies to protect lower-income enrollees. But for middle-income households, the financial hit can be steep. A 55-year-old couple in Redding earning $107,000 per year, for example, could face an extra $2,165 per month with no federal subsidy cushion.

This guide breaks down exactly what drives your premium, what’s changed, and how to find the most affordable plan for your situation.

Understanding Covered CA Rates in 2026

When we look at the landscape of health insurance in 2026, the baseline numbers tell an interesting story. On one hand, Covered California has done an admirable job of negotiating with major insurance carriers. The preliminary weighted average rate increase for covered ca rates is 10.3% for the 2026 coverage year.

While a double-digit rate hike is never fun to talk about, it looks incredibly stable when compared to the rest of the country. Nationally, average health insurance rates are projected to spike by a staggering 20% in 2026. This lower rate change in California is a testament to the state’s large, stable risk pool and active negotiation by marketplace officials.

However, the real-world impact on your wallet depends heavily on whether you qualify for financial assistance. Because California reached a record-high enrollment of 1,927,520 active members in early 2025, any shift in pricing structures affects millions of our neighbors.

If you are worried about how these baseline increases will translate to your monthly bank statement, you are not alone. To understand how base rates turn into your actual monthly bill, it helps to read our guide on everything you need to know about health insurance cost per month in california.

To see the official announcement and the state’s positioning on these changes, you can review the Covered California Rates And Plans For 2026 Consumer Affordability On The Line With Uncertainty Surrounding Federal Premium Tax Credit Extension.

The Expiration of Federal Subsidies and the Impact on Your Premium

The elephant in the room for 2026 is the expiration of the enhanced federal premium tax credits, which officially sunsetted on December 31, 2025. Introduced during the pandemic, these enhanced subsidies did two incredibly important things:

- They capped health insurance premiums at 8.5% of a household’s income.

- They extended financial help to middle-income families earning more than 400% of the Federal Poverty Level (FPL).

With these enhanced subsidies gone, federal assistance has reverted to traditional, pre-pandemic Affordable Care Act (ACA) levels. This creates a massive $2.1 billion federal funding gap in California alone.

Without these enhanced credits, an estimated 1.7 million California enrollees face an average net premium increase of 66%. Middle-income families who previously enjoyed capped premiums are now feeling the full weight of unsubsidized market rates. For instance, consumer responsibility under the standard subsidy calculation has risen from a maximum of 7.08% of household income up to 9.78%, severely reducing the size of the monthly tax credits.

How Federal Policy Changes Affect Covered CA Rates

The loss of enhanced subsidies is not the only federal policy shift making waves in 2026. We are also adapting to several structural changes in how health insurance is administered:

- Shortened Open Enrollment Period: Starting in 2026, the open enrollment window is tighter. It now runs from November 1 to December 31 for coverage starting January 1, 2027. This is a departure from previous years when Californians had until January 31 to finalize their plans.

- Bronze Plans as HDHPs: In a bit of good news, Bronze and minimum coverage plans now qualify as High-Deductible Health Plans (HDHPs). This means enrollees can finally pair these plans with a tax-advantaged Health Savings Account (HSA) to pay for out-of-pocket medical expenses.

- DACA Recipient Eligibility: Deferred Action for Childhood Arrivals (DACA) recipients remain eligible to enroll in marketplace plans with financial assistance, protecting access to vital services.

- Gender-Affirming Care: Despite various federal policy shifts, California state law continues to mandate that all Covered California plans cover gender-affirming care.

For a comprehensive breakdown of these regulatory updates, visit the official Important Changes – Covered California page.

State-Funded Subsidies to Offset Rising Covered CA Rates

Recognizing the financial cliff facing residents, the California state government has stepped in to soften the blow. For the 2026 plan year, California has allocated $190 million in state-funded subsidies.

While $190 million is a massive investment, it cannot entirely fill the $2.1 billion federal funding gap. Therefore, the state has highly targeted this assistance to protect the most vulnerable. These state subsidies are designed to keep premiums comparable to 2025 levels specifically for individuals and families earning up to 150% of the Federal Poverty Level (FPL).

Additionally, California continues to support its enhanced Cost-Sharing Reduction (CSR) program, utilizing a previously appropriated $165 million to lower deductibles and copays for qualifying Silver-tier plans. To see how these state-level programs lower your personalized pricing, read our breakdown of covered california estimated cost.

How Premium Costs Vary Across California

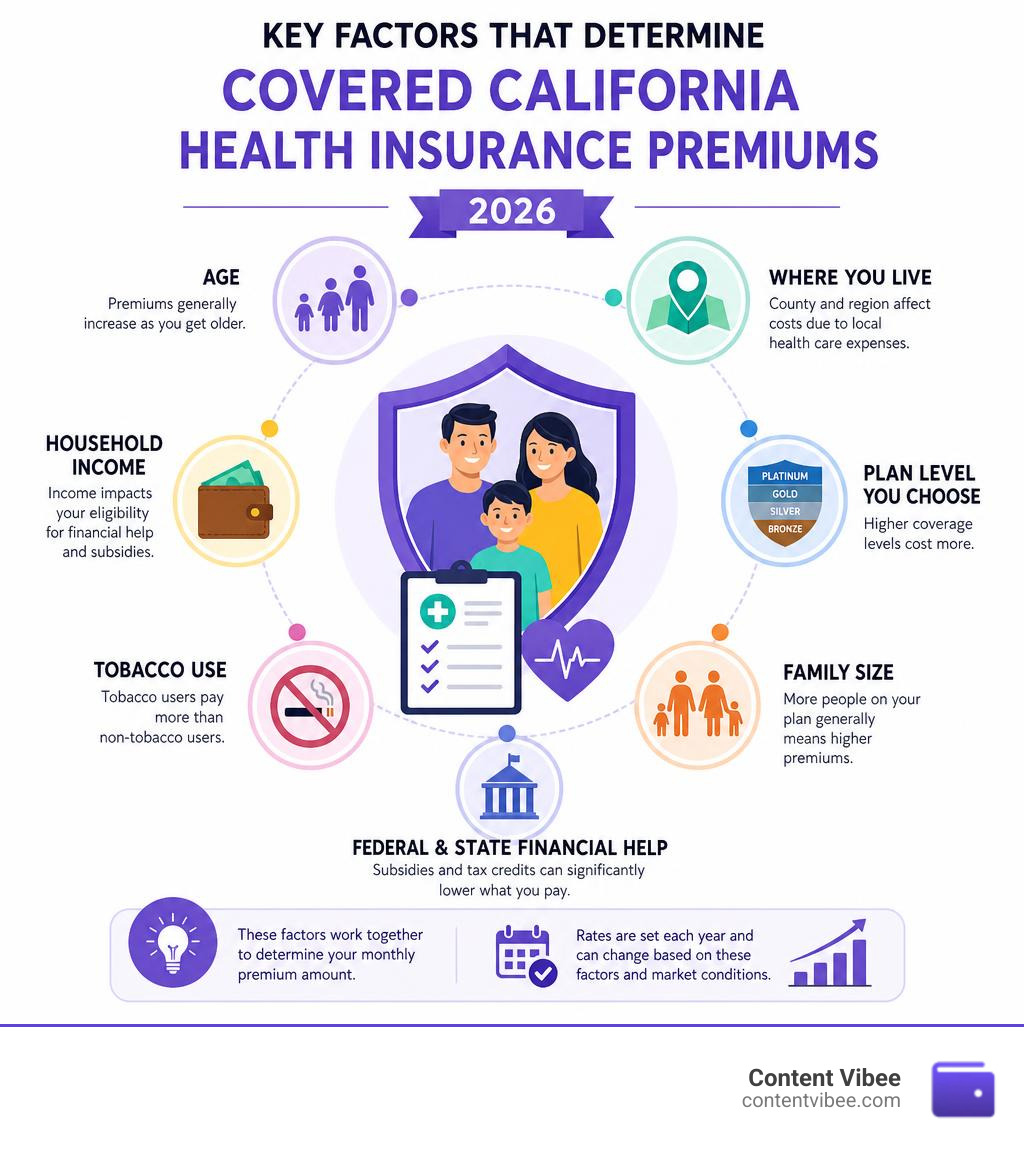

One of the most common points of confusion we see is why two people with the same income can pay wildly different covered ca rates. Your monthly health insurance cost is determined by a combination of four major factors:

- Age: Older individuals generally pay higher premiums than younger individuals for the same plan, up to a federal limit of a 3-to-1 ratio.

- Income & Household Size: These two factors dictate your Federal Poverty Level (FPL) percentage, which determines your subsidy eligibility.

- Geographic Region: California is divided into 19 rating regions. Insurance companies price their plans based on local healthcare costs and carrier competition in those specific regions.

- Metal Tier Selection: The balance between monthly premium costs and out-of-pocket expenses when you receive care.

Geographic variation is particularly stark in 2026. For example, Region 11 (Fresno, Kings, and Madera counties) and Region 13 (Imperial, Inyo, and Mono counties) saw the highest average rate increases in the state at 12.9%. Meanwhile, urban areas with more hospital competition often see much lower average increases.

Real-World Examples of 2026 Premium Costs

To put these abstract percentages into perspective, let’s look at how actual Californians across different brackets and regions are affected in 2026:

- The Young Professional (Sacramento): A 40-year-old single individual earning $31,300 per year in Sacramento County faces a benchmark Silver plan premium of $638 per month before subsidies. Thanks to tax credits, they receive a monthly Advance Premium Tax Credit (APTC) of $467, bringing their net premium down to $171 per month (plus a $1 state premium credit adjustment).

- The Middle-Income Couple (Redding): John and Louise, a 55-year-old couple in Redding earning $107,000 per year, no longer qualify for federal subsidies due to the expiration of the enhanced tax credits. They face an astronomical premium increase of $2,165 per month, forcing them to pay full price for their coverage.

- The Gig Worker (Los Angeles): Kevin, a 25-year-old rideshare driver earning $32,000 per year, sees his monthly premium triple from a subsidized $50/month in 2025 to $172 per month in 2026.

| Demographic Profile | Location | Household Income | 2026 Net Monthly Premium (Silver Plan) |

|---|---|---|---|

| 40-Year-Old Single | Sacramento | $31,300 | $171 / month |

| 25-Year-Old Single | Los Angeles | $32,000 | $172 / month |

| Single Parent (1 Child) | Bay Area | $43,000 | $233 / month |

| 55-Year-Old Couple | Redding | $107,000 | Full Price (+$2,165/month change) |

For families trying to navigate these regional pricing changes together, we recommend checking out the ultimate guide to family health insurance plans for tailored strategies on bundling coverage.

Choosing the Right Plan: Metal Tiers and Carrier Options

When shopping for health insurance, you will choose from four “metal tiers” that categorize how you and your plan share costs.

- Bronze: Has the lowest monthly premiums but the highest out-of-pocket costs when you need care. These are excellent for healthy individuals who only want protection against major medical emergencies.

- Silver: The “benchmark” tier. If you qualify for cost-sharing reductions, you must choose a Silver plan to receive those lowered deductibles and copays.

- Gold: Higher monthly premiums, but the plan pays a larger share of your medical costs (usually around 80%).

- Platinum: The highest monthly premiums but virtually no deductibles and very low copays. Ideal for those who require frequent medical services or expensive prescriptions.

Beyond metal tiers, you must choose a network type:

- HMO (Health Maintenance Organization): Requires you to use network doctors and get referrals from a primary care physician (PCP), but offers the lowest out-of-pocket costs.

- PPO (Preferred Provider Organization): Gives you the freedom to see any doctor without a referral, including out-of-network providers, but comes with higher premiums.

- EPO (Exclusive Provider Organization): A hybrid network where you don’t need referrals, but the plan will not pay for any out-of-network care.

Carrier Competition and Plan Availability in 2026

For 2026, there are 11 health insurance companies participating in the Covered California marketplace. The good news is that competition remains robust: 92% of Californians have a choice of three or more carriers, and 75% can choose from four or more.

However, carrier participation varies by region. The biggest market disruption in 2026 is Aetna’s exit from the California exchange, which impacts nearly 21,000 enrollees across four regions. If you were enrolled with Aetna, you must actively select a new carrier during the open enrollment window to avoid being automatically transitioned to a default plan.

Carrier rate increases also vary significantly. For example, Kaiser Permanente negotiated a relatively low average rate increase of 7.1%, while Valley Health Plan in Santa Clara County experienced the highest average increase at 21.0%.

To see how these carriers stack up against each other in terms of network size and customer satisfaction, check out a comprehensive guide to health insurance plans comparison.

Actionable Steps to Lower Your Health Insurance Costs

While the headline rate increases and subsidy expirations sound intimidating, you are not powerless. We have identified several concrete steps you can take to keep your health coverage affordable:

- Shop and Switch: This is the single most effective tool at your disposal. If you stay with your current plan, you will feel the full force of the 10.3% rate increase. However, if you “shop and switch” to the lowest-cost plan in your current metal tier, the average statewide rate change drops to just 1.0%.

- Verify Your Income Accurately: Underestimating your income can lead to a painful tax bill at the end of the year when the IRS clawbacks overpaid subsidies. Overestimating your income means you will pay too much for your premium each month. Keep your application updated with any job changes.

- Utilize the Shop and Compare Tool: Before making any decisions, input your ZIP code, household size, and estimated income into the Covered California online tool to see exactly what subsidies you qualify for.

If you are ready to make a change but want to make sure you don’t miss any critical deadlines, read our walkthrough on the easiest way to enroll in health insurance.

Frequently Asked Questions about California Health Insurance

What is the average rate increase for Covered California in 2026?

The preliminary weighted average rate increase for Covered California plans in 2026 is 10.3%. This is significantly lower than the projected national average rate increase of 20%, thanks to California’s highly competitive marketplace and large pool of active enrollees.

How do I know if I qualify for state-funded subsidies?

State-funded subsidies for 2026 are primarily targeted at lower-income individuals and families earning up to 150% of the Federal Poverty Level (FPL). To see if your household income falls within this threshold, you can use the Shop and Compare Tool on the Covered California website or contact a certified enrollment counselor.

What happens if I do not enroll during the open enrollment period?

If you miss the shortened open enrollment window (which runs from November 1 to December 31), you cannot sign up for a plan unless you qualify for a Special Enrollment Period (SEP). Qualifying life events for an SEP include losing job-based insurance, getting married, having a baby, or permanently moving to a new ZIP code.

Conclusion

Navigating the shifting waters of covered ca rates in 2026 requires a proactive approach. The loss of enhanced federal subsidies is a real challenge for middle-income Californians, but with state-targeted relief and a highly competitive local market, affordable options are still within reach.

By understanding your options, comparing metal tiers, and being willing to shop around, you can protect both your physical health and your financial peace of mind. For more expert personal finance tips and health insurance breakdowns, explore our complete guide on everything you need to know about health insurance cost per month in california.