The Ultimate Guide to Paying Medical Bills After a Car Wreck

When the Bills Arrive Before the Settlement Does

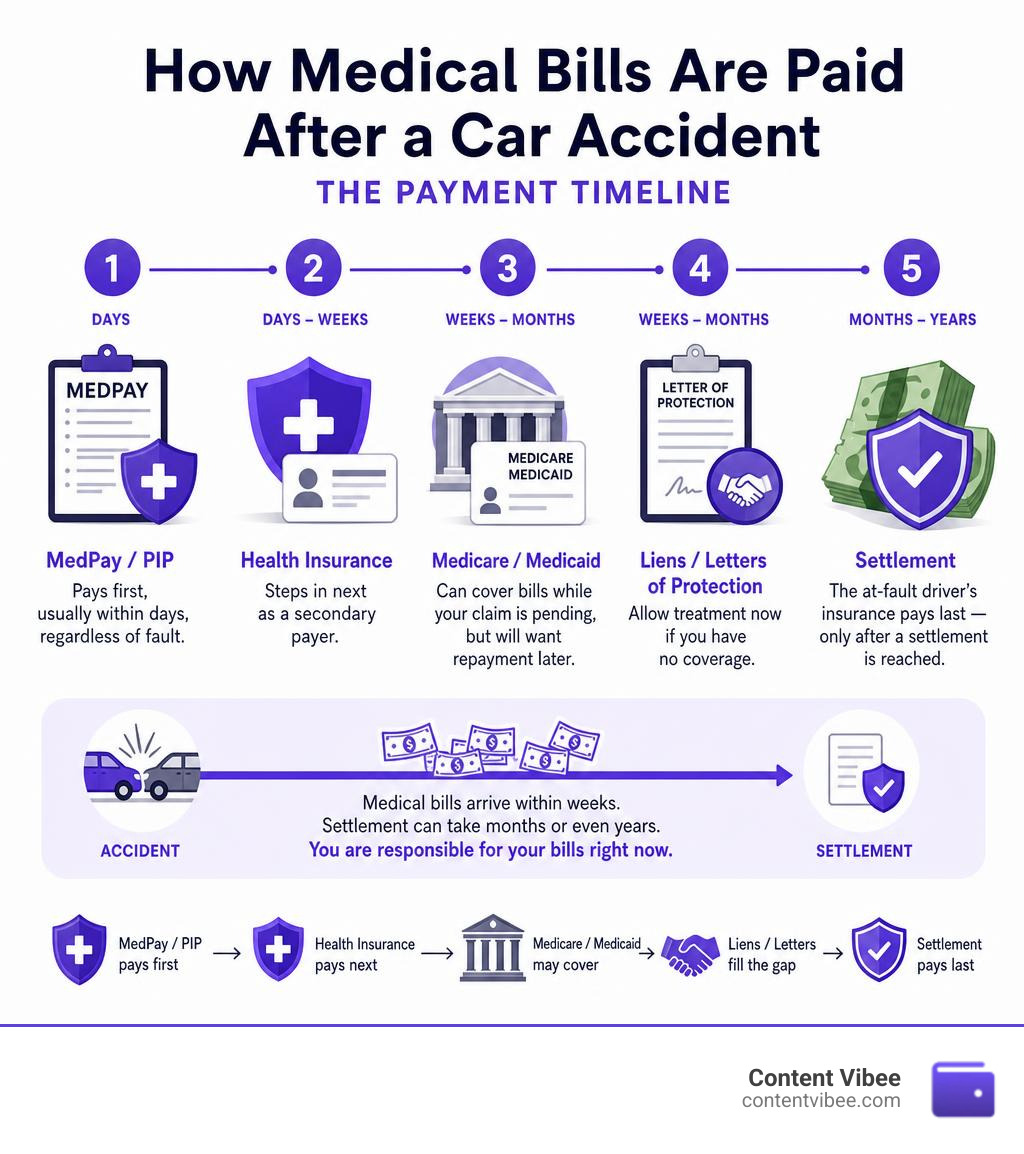

Understanding how medical bills are paid after a car accident is one of the most urgent questions injured drivers face — and the answer isn’t simple.

Here’s the short version:

- MedPay or PIP (if you have it) pays first, usually within days, regardless of fault

- Your health insurance steps in next as a secondary payer

- Medicare or Medicaid can cover bills while your claim is pending, but will want repayment later

- Medical liens / letters of protection allow treatment now if you have no coverage

- The at-fault driver’s insurance pays last — only after a settlement is reached, which can take months or even years

The core problem? The hospital bills you within weeks. The settlement takes much longer.

Average bodily injury claims now run $29,400 — up 81% since 2016. For serious injuries, costs can climb into the hundreds of thousands. And large medical bills are one of the leading causes of personal bankruptcy in the United States.

You are still responsible for your bills right now, even if someone else caused the crash. Insurance companies don’t pay providers visit by visit. They pay once, at the end — and that gap between the accident and the settlement is where most of the financial stress lives.

This guide walks you through every step: who pays first, what happens if you’re uninsured, how subrogation and liens work, and how to protect yourself from ending up with less money than you owe.

The Immediate Dilemma: How Medical Bills Are Paid After Car Accident While a Claim is Pending

When you are wheeled into an emergency room after a crash, the hospital staff is focused on stabilizing you. However, once you are discharged, the administrative wheels start turning. You will likely receive invoices from the hospital, the attending physician, the radiology department, and the ambulance service.

At this stage, many people make the mistake of sending these bills directly to the at-fault driver’s auto insurance company, expecting them to be paid immediately. Unfortunately, that is not how liability insurance works.

The negligent driver’s insurance provider will not pay your medical bills as they come in. They do not write checks to your physical therapist or your pharmacist. Instead, they wait until you have finished all medical treatment so they can offer a single, one-time lump-sum settlement. This settlement is designed to cover all your damages at once—including past medical bills, future care, lost wages, and pain and suffering.

Because a personal injury claim can take anywhere from six months to several years to fully resolve, you need a strategy to handle these costs in the interim. If you simply let the bills sit, they will eventually be sent to collections, which can severely damage your credit rating. Understanding the sequence of payment sources is essential to keeping your finances intact while your case is pending. For a deep dive into the breakdown of these immediate expenses, you can explore this resource on Car Accident Medical Costs — How Bills Get Paid.

The Payment Hierarchy: Who Pays First?

To keep your bills from going to collections, you must navigate a specific payment hierarchy. Depending on your state and your individual insurance policies, different coverages will act as the “primary” or “secondary” payers.

Here is a quick look at how these coverages typically stack up:

| Coverage Type | Priority Level | What It Covers | Who Pays the Deductible? |

|---|---|---|---|

| Personal Injury Protection (PIP) | Primary (in No-Fault states) | Medical bills, lost wages, and sometimes funeral costs regardless of fault. | You (if your policy has a deductible). |

| Medical Payments (MedPay) | Primary (in At-Fault states, if purchased) | Direct medical and funeral expenses for you and your passengers. | Usually $0 deductible. |

| Private Health Insurance | Secondary (pays after PIP/MedPay are exhausted) | Standard covered medical treatments within your network. | You (subject to your health plan’s deductible/copays). |

| At-Fault Liability Insurance | Tertiary (pays last, at settlement) | Lump-sum reimbursement for all medical costs, lost wages, and pain and suffering. | No deductible for you, but limited by the at-fault driver’s policy cap. |

Understanding How Medical Bills Are Paid After Car Accident in No-Fault vs. At-Fault States

The rules governing how medical bills are paid after a car accident depend heavily on whether you live in a “no-fault” or an “at-fault” (tort) state.

- No-Fault States: In states with no-fault insurance laws, your own auto insurance company is required to pay for your medical treatments up to a certain limit, regardless of who caused the wreck. This coverage is known as Personal Injury Protection (PIP). In these states, you must exhaust your PIP limits before you can file a claim against the at-fault driver’s insurance or use your private health insurance.

- At-Fault States: In traditional tort or “at-fault” states, the driver who caused the accident is legally responsible for the damages. However, because their insurance won’t pay until a final settlement is reached, you must rely on your own coverage sources—such as MedPay or private health insurance—to cover costs while your claim is pending. Once the case settles, the at-fault driver’s insurance will reimburse those costs (or pay off outstanding medical liens).

Primary Coverage Sources for Accident-Related Healthcare

Managing your physical recovery means coordinating several different insurance policies. Let’s look closely at the primary coverage sources you will use to pay your bills.

Personal Injury Protection (PIP) and Medical Payments (MedPay) Coverage

PIP and MedPay are specialized auto insurance coverages designed specifically for accident-related medical expenses.

- Personal Injury Protection (PIP): PIP is highly comprehensive. It typically covers 80% to 100% of your medical bills and can also reimburse you for lost wages if your injuries prevent you from working. In some states, PIP benefits require an “Emergency Medical Condition” (EMC) attestation from a doctor to unlock the full policy limits. Without an EMC, your benefits might be capped at a much lower amount (for example, $2,500 instead of $10,000).

- Medical Payments (MedPay): MedPay is an optional, budget-friendly add-on in many states. Unlike PIP, it does not cover lost wages, but it is excellent for covering out-of-pocket medical costs like deductibles and health insurance copays. MedPay policies typically range from $1,000 to $10,000 in coverage and usually carry no deductible.

To understand more about how these auto policy features interact with healthcare providers, check out this guide on How Medical Bills Are Paid After an Auto Accident.

Using Private Health Insurance After a Crash

Once your MedPay or PIP limits are completely exhausted (or if you don’t have these coverages), your private health insurance is the next line of defense.

Many people hesitate to use their health insurance because they feel the at-fault driver should pay. However, using your health insurance is highly beneficial. Health insurance companies have pre-negotiated, discounted rates with healthcare providers. A hospital bill that nominally costs $10,000 might be reduced to $3,000 under a health insurance contract.

You will still be responsible for your standard deductibles, copays, and coinsurance, but using this coverage keeps the bills paid and protects your credit score. If you eventually receive a settlement from the at-fault driver, your health insurance provider may seek reimbursement for what they paid—a process called subrogation, which we will cover below.

Government Programs: Medicare, Medicaid, and Tricare

If you are covered by Medicare, Medicaid, or military insurance like Tricare, these programs can also pay for your accident-related treatments.

However, federal and state laws designate these programs as “secondary payers.” This means they will only pay after any available auto insurance (like PIP or MedPay) has been fully exhausted.

Furthermore, government programs have incredibly strict, legally protected reimbursement rights. If Medicare or Medicaid pays for your treatments and you later win a settlement, they will place a “super lien” on your recovery. You are legally required to pay them back from your settlement funds before you can keep any of the money.

What Options Exist If You Are Uninsured or Underinsured?

If you do not have health insurance and your auto policy lacks PIP or MedPay, finding yourself with injuries after a crash can feel terrifying. Nationally, about 15.4% of drivers are uninsured, and many more lack sufficient health coverage. Fortunately, you still have options to receive quality care.

Hospital Liens and Letters of Protection (LOP)

If you do not have the means to pay upfront, your attorney can help you secure treatment through specialized legal agreements.

- Letter of Protection (LOP): A Letter of Protection is a legally binding agreement sent by your personal injury lawyer to your medical providers. The LOP promises that the medical provider will be paid directly out of your future settlement. In exchange, the provider agrees to treat you now and delay all billing and collection efforts until your case is resolved.

- Hospital Liens: In some states, hospitals have a statutory right to file a lien against your future personal injury settlement or verdict if they provide emergency care. This lien is filed in county property records. It ensures that when the at-fault insurance company finally issues a settlement check, the hospital is paid directly from those proceeds before the remaining funds are distributed to you.

Negotiating Medical Bills and Setting Up Payment Plans

If you must pay out of pocket, medical bills are rarely set in stone. Healthcare providers are often willing to work with uninsured patients to avoid sending accounts to collections.

We recommend using the following negotiation strategies:

- Request an Itemized Statement: Ask for a fully itemized bill with CPT (Current Procedural Terminology) codes. Hospitals frequently make billing errors, such as double-billing for supplies or charging for services you never received.

- Ask for a “Self-Pay” Discount: Many hospitals and clinics will slash your bill by 30% to 50% if you tell them you are paying out of pocket without insurance.

- Apply for Financial Assistance: Non-profit hospitals are federally required to offer financial assistance programs (often called “charity care”) to low-income patients.

- Establish an Interest-Free Payment Plan: If you cannot pay the full balance, ask to set up a monthly payment plan. Even paying as little as $20 to $50 a month can keep your account in good standing and out of collections.

The Settlement Phase: Subrogation, Liens, and Reimbursement

Once you reach “Maximum Medical Improvement” (meaning your injuries have healed as much as they are expected to), your attorney will begin negotiating a settlement with the at-fault driver’s insurance company.

However, signing a settlement agreement does not mean you get to pocket the entire check. Before you receive your share, all outstanding medical bills, hospital liens, and insurance reimbursement claims must be satisfied.

How Subrogation Works After a Settlement

Subrogation is a legal process that prevents “double-dipping.” If your health insurance company paid $20,000 for your surgery, and you later recover that same $20,000 from the at-fault driver’s auto insurance, you cannot keep that money. Your health insurer has a right to be paid back because the negligent party is ultimately responsible for the bill.

During the settlement phase, your attorney will receive a subrogation demand from your health insurance company. A skilled lawyer will review this demand line by line to ensure the insurer is only charging you for treatments directly related to the accident. They will also negotiate to reduce the subrogation amount, often saving you thousands of dollars. To understand how this fits into the broader settlement timeline, read our comprehensive Car Accident Settlement Guide 2026.

Can You Be Held Responsible for Unpaid Bills If the Settlement Is Too Low?

Yes. This is one of the most critical risks of handling a claim without legal guidance.

If the at-fault driver only carries their state’s minimum liability limits (which can be as low as $15,000 or $25,000 in some states), and your medical bills total $100,000, the settlement check will not cover what you owe.

Because you signed a contract with the hospital to pay for your care, you remain personally liable for any unpaid medical balances even after your settlement is completely gone. To avoid this financial trap, it is vital to understand the true value of your claim before accepting any early offers. You can learn more about valuing your case in our Az Guide To How Much Is My Car Accident Settlement Worth.

How Legal Representation Helps Coordinate Payments and Maximize Recovery

Trying to negotiate with insurance adjusters while recovering from physical injuries is incredibly difficult. Insurance companies are businesses, and their primary goal is to settle your claim for as little money as possible. Hiring an experienced attorney can completely change the outcome of your recovery.

How Medical Bills Are Paid After Car Accident with the Help of an Attorney

An attorney does far more than just file lawsuits. They act as a financial buffer between you and your medical providers.

Your lawyer will coordinate with your doctors, submit Letters of Protection to prevent collections, and handle all subrogation negotiations. In many cases, an attorney can negotiate outstanding hospital liens down by 30% to 50%, leaving more settlement money in your pocket.

If you are worried about the cost of legal help, you should know that personal injury lawyers work on a contingency fee basis—meaning they only get paid if they win your case. For a clear breakdown of how these fees work, read our guides on How Much Does A Personal Injury Lawyer Cost and How To Find A Good Car Accident Lawyer.

Calculating Your Total Damages for a Fair Settlement

To secure a settlement that actually covers your bills, your attorney will calculate both your economic and noneconomic damages.

- Economic Damages: These are objective, quantifiable financial losses. They include emergency room fees, doctor visits, physical therapy, prescription medications, future medical treatments, and lost wages.

- Noneconomic Damages: These are subjective losses, such as physical pain and suffering, emotional distress, loss of enjoyment of life, and mental anguish.

To estimate what your potential recovery might look like based on your specific injuries and bills, you can use our interactive Car Accident Settlement Calculator.

Frequently Asked Questions about Car Accident Medical Bills

How long does it take for the at-fault driver’s insurance to pay my medical bills?

The at-fault driver’s insurance will not pay your bills as they arrive. They will only pay at the very end of your case via a lump-sum settlement. This process typically takes anywhere from 6 months to over 3 years, depending on the complexity of the accident, the length of your medical treatment, and whether a lawsuit must be filed.

Can medical bills from a car accident ruin my credit score?

Yes, if they are left unpaid and go to collections. To protect your credit, you should always submit your bills to your PIP, MedPay, or private health insurance immediately. If you have no insurance, have your attorney establish a Letter of Protection (LOP) with your providers to halt all collection efforts while your claim is pending.

What is the average medical bill for a car accident injury?

The average bodily injury claim in 2026 is estimated at $29,400. However, medical costs vary widely. A minor whiplash injury requiring chiropractic care might cost between $2,500 and $10,000, while severe injuries involving surgeries, emergency transport, and long-term rehabilitation can easily exceed $100,000 or even $1,000,000.

Conclusion

Navigating the financial aftermath of a car crash is a multi-layered process. From coordinating PIP and health insurance to negotiating medical liens and subrogation demands, the decisions you make in the weeks following an accident can impact your personal finance for years to come.

At Content Vibee, we believe that smart financial recovery starts with education. You do not have to navigate this overwhelming system alone. Working with an experienced personal injury attorney is often the best way to protect your credit, reduce your medical debt, and secure the compensation you deserve. To learn more about how legal fees are structured and how they impact your final payout, read our guide on How Much Do Lawyers Charge For Accident Claims.