The Ultimate Guide to Handling an Auto Insurance Claim Denial

What to Do When Your Auto Insurance Claim Is Denied

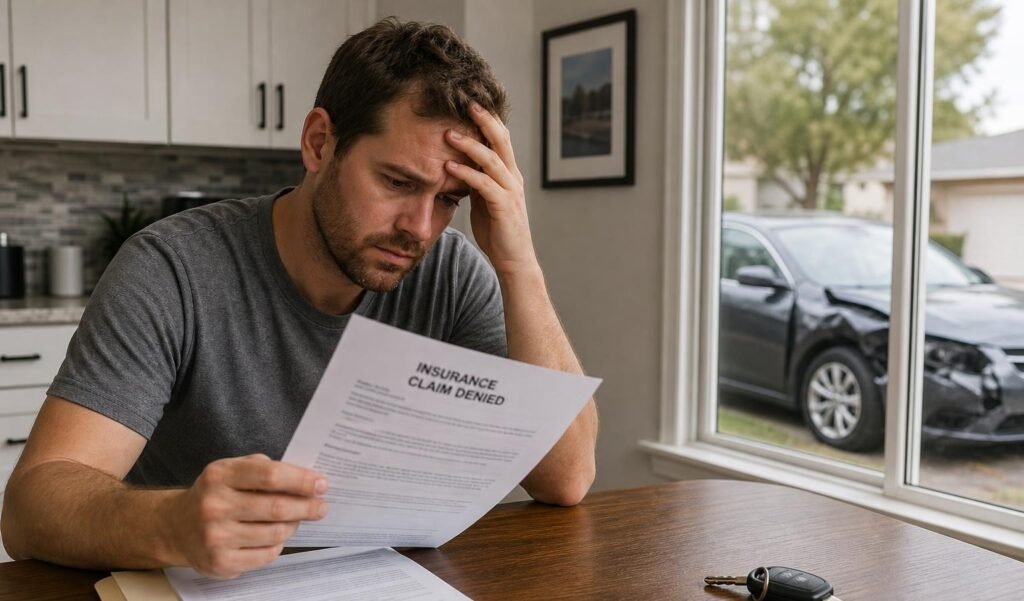

Having your auto insurance claim denied is frustrating u2014 especially when you’re already dealing with a wrecked car, medical bills, and missed work. But a denial letter is not the end of the road.

Here’s what to do right away if your claim was denied:

- Read the denial letter carefully u2014 find the exact reason given

- Check your policy u2014 compare the denial reason to your actual coverage

- Gather evidence u2014 police report, photos, medical records, repair estimates

- Write a formal appeal letter u2014 address each reason for denial with documentation

- Send via certified mail u2014 keep a paper trail of everything

- Escalate if needed u2014 file a complaint with your state’s insurance department or consult an attorney

Most states require insurers to respond to appeals within 30 to 60 days. Many denials are successfully reversed when new or overlooked evidence is submitted.

You paid for coverage. You have the right to fight for it.

Roughly 14% of U.S. drivers are uninsured, which means even careful drivers can end up in complicated claim situations u2014 especially when the at-fault driver has no coverage. Add in policy exclusions, missed deadlines, and fault disputes, and it’s easy to see why denials happen more often than most people expect.

This guide walks you through exactly what to do, step by step.

Why Was Your Auto Insurance Claim Denied?

When we open that official-looking envelope and see the word “denied,” it can feel like a personal insult. However, from the insurance company’s perspective, a claim denial is a business decision based on policy language, contract terms, and available evidence.

To successfully challenge a denial, we first have to understand the rules of the game. The first major distinction is whether you filed a first-party claim or a third-party claim. How the insurer handles your claimu2014and your legal rights during the disputeu2014depends heavily on this classification.

| Feature | First-Party Claim | Third-Party Claim |

|---|---|---|

| Who files it? | You (the policyholder) | You (against another driver’s insurer) |

| Basis of Claim | Your own insurance contract | The other driver’s liability policy |

| Contractual Duty | Yes, the insurer owes you a duty of good faith | No contractual relationship exists |

| Denial Rate | Lower (regulated more strictly) | Higher (insurers look to protect their bottom line) |

| Bad Faith Lawsuits | Available in most states | Generally not available (with some exceptions) |

If you are dealing with a complex coverage dispute or need to know your rights under national regulatory frameworks, you can learn more about consumer protections from the NAIC by reviewing What Can I Do If My Car Insurance Denies My Claim? .

Common Reasons for Claim Rejection

Insurance companies use a structured taxonomy to evaluate and, in some cases, reject claims. Here are the most common reasons why an auto insurance claim denied letter might land in your mailbox:

- Lapsed Policy: This is the most common administrative reason for a denial. If you missed a premium payment and your policy’s grace period expired, you were driving without coverage at the time of the accident.

- Excluded Drivers: If you let a friend, family member, or partner drive your car, but they are explicitly excluded from your policy (or not listed as an authorized driver in households where that is required), the carrier will deny coverage for any accident they cause.

- Pre-Existing Damage: If an insurance adjuster inspects your vehicle and determines that the dent, scratch, or mechanical failure was present before the collision, they will refuse to pay for that portion of the repairs.

- Insufficient Coverage Limits: If your vehicle sustained $30,000 in property damage but your policy limit for collision coverage is capped at $25,000, the insurer will deny payment for the remaining $5,000. To avoid running into these limits, it is always wise to proactively research and secure adequate policies. You can read our guide to cheap auto insurance quotes to learn how to balance affordable rates with robust coverage limits.

- Disputes Over Fault: If your statement contradicts the other driveru2019s statement, and there is no clear physical evidence or police report to break the tie, the insurer may deny liability altogether.

First-Party vs. Third-Party Claim Denials

First-party claims are filed with your own insurance company (e.g., under your collision, comprehensive, or medical payments coverage). Because you pay premiums to them, they owe you a contractual duty of good faith and fair dealing. If they deny your claim without a reasonable basis or fail to conduct a thorough investigation, you may have grounds for a bad faith lawsuit.

Third-party claims are filed against the insurance provider of the at-fault driver. Because you do not have a contract with that insurance company, they do not owe you a direct duty of good faith. In fact, in states like California, landmark legal rulings such as Moradi-Shalal v. Firemanu2019s Fund prevent third-party claimants from filing bad faith lawsuits directly against another driver’s insurer. This means third-party claims are denied at a significantly higher rate, as carriers know they face fewer regulatory penalties for denying non-customers.

To see how claims are handled across different regions, you can check out the States With the Highest Auto Insurance Claim Denials database provided by the National Association of Insurance Commissioners.

How to Appeal a Denied Car Insurance Claim

If your claim is rejected, do not panic. A denial is simply the insurer’s initial decisionu2014it is not the final verdict. You have the right to initiate an internal appeal, which forces a supervisor or a separate appeals committee to review your case.

The appeals process operates on a strict timeline, typically requiring you to submit your appeal within 30 to 60 days of receiving the denial. For a comprehensive overview of how to navigate these industry-standard timelines, you can refer to What to Do When Your Insurance Claim Is Denied: A Step-by-Step Guide.

What to Do When Your Auto Insurance Claim Denied Letter Arrives

The moment you open your denial letter, your focus should shift to strategy. Here are the immediate steps we recommend taking:

- Pinpoint the Deadline: Look for the date on the letter and locate the section detailing your appeal window. Mark this date in bold red on your calendar. Missing this deadline can permanently forfeit your right to dispute the decision.

- Analyze the Cited Policy Language: Insurers are legally required to provide a written explanation citing the exact policy provisions, exclusions, or conditions they used to justify the denial. Locate your original policy declarations page and read those specific sections word for word.

- Check for Simple Clerical Errors: Sometimes, claims are denied simply because of a misspelled name, an incorrect vehicle identification number (VIN), or a transposed digit in your policy number.

- Reach Out to Your Carrier: If the letter is written in confusing legal jargon, call your insurance provider directly to ask for a plain-English explanation. If you are insured with a major carrier, having their direct contact info handy is crucial. For example, you can find the general car insurance phone number in our directory to get connected with customer service quickly.

Step-by-Step Appeal Process

Once you understand why the claim was denied, it is time to build your appeal package. Follow this step-by-step process to maximize your chances of reversing the decision:

- Step 1: Write a Formal Appeal Letter: Keep your tone calm, professional, and strictly factual. Avoid emotional pleas. Address each reason cited in the denial letter individually, using objective evidence to disprove the insurer’s claims.

- Step 2: Assemble Your Evidence Packet: Organize your supporting documents (such as police reports, repair shop diagnostics, and photos) into clearly labeled exhibits.

- Step 3: Submit via Certified Mail: Always send your appeal package via certified mail with a return receipt requested. This provides legal proof of the exact date the insurer received your appeal.

- Step 4: Monitor the Response Window: Under the National Association of Insurance Commissioners (NAIC) model act, insurers are typically required to acknowledge your appeal and provide a formal response within 21 to 45 days.

To learn more about drafting a persuasive appeal letter and navigating this process, you can read How to Appeal a Denied Auto Insurance Claim: Steps to Take.

Gathering the Right Evidence for Your Appeal

An appeal without evidence is just an opinionu2014and insurance companies do not pay out on opinions. To win your appeal, you must present an organized, undeniable wall of proof.

Essential Documentation to Collect

To overturn an auto insurance claim denied decision, you should gather and organize the following essential documents:

- The Official Police Report: If the responding officer determined that the other driver was at fault or issued them a citation, this is incredibly powerful evidence that is very difficult for an insurer to dispute.

- Comprehensive Photographic Evidence: Provide clear, high-resolution photos of the accident scene, the damage to all involved vehicles, skid marks, road hazards, and any relevant traffic signs.

- Detailed Repair Estimates: Get written, itemized repair estimates from at least two independent, reputable auto body shops to prove the physical extent and financial cost of the damage.

- Meticulous Medical Records: If your claim involves bodily injury, gather all medical charts, diagnostic imaging (like X-rays or MRIs), and bills that directly link your injuries to the collision.

- Witness Statements & Dashcam Footage: Objective, third-party accounts or video recordings of the actual collision are the gold standard of evidence.

If you find yourself needing to switch to a carrier with a better reputation for fair claim handling, you can easily compare car insurance quotes using our free online tool.

Challenging AI-Driven Claims Decisions

In May 2026, many major insurance carriers rely heavily on artificial intelligence algorithms to process claims. While this speeds up simple claims, it also leads to automated denials. AI software often misclassifies fresh collision damage as “prior wear-and-tear” or automatically rejects claims if a document is uploaded with minor formatting issues.

If you suspect your claim was rejected by an algorithm, write a formal letter demanding an immediate human review of your file. Highlight any specific nuances of the accident that a computer algorithm would easily overlook. For a detailed guide on how to spot and challenge these automated decisions, check out Insurance Denial Letter: A Step-by-Step Appeal Guide.

Legal Options and Escalation Strategies

If your internal appeal is rejected, do not lose hope. You still have several powerful escalation strategies to force the insurance company to pay what you are owed.

When to Hire an Attorney for an Auto Insurance Claim Denied

You do not always need a lawyer to appeal a minor property damage claim. However, we highly recommend hiring an experienced personal injury or insurance dispute attorney if:

- You sustained severe or permanent injuries.

- Your medical bills and lost wages total thousands of dollars.

- The insurance company is completely unresponsive or acting in bad faith.

- The policy language is highly complex or ambiguous.

Most reputable auto accident attorneys work on a contingency fee basis. This means they do not charge any upfront legal fees; instead, they only take a percentage of the final settlement they win for you. For professional legal advice on how to proceed, you can read Car Insurance Claim Denied? What to Do Next.

Filing a State Insurance Department Complaint

Every state has an insurance commissioner who oversees all insurance companies operating within their borders. If your insurer is violating state laws or refusing to cooperate during your appeal, you can file a formal complaint with your state’s Department of Insurance (DOI).

Under state Unfair Claim Settlement Practices Acts (UCSPA), regulators have the power to investigate your claim, audit the insurer’s files, and levy heavy fines if they find patterns of unfair denials. Filing a complaint is entirely free and puts immediate regulatory pressure on the carrier. To find your state’s specific regulatory agency, consult the Insurance Claim Denied: The 5 Reasons Carriers Use, the 30-60-90 Day Appeal Timeline, and When to File with the Commissioner directory.

Bad Faith Insurance Practices

Insurers have a legal “duty of good faith and fair dealing” to their policyholders. If your own insurance provider commits any of the following acts, they may be guilty of bad faith:

- Denying a claim without conducting a fair, thorough, and unbiased investigation.

- Intentionally delaying claim processing or communication to pressure you into a low settlement.

- Refusing to provide a clear, written explanation of the factual and legal basis for a denial.

- Offering a settlement amount that is substantially lower than independent repair estimates without a valid explanation.

If bad faith is proven in court, you may be awarded damages far exceeding your original policy limits, including compensation for emotional distress and punitive damages. To learn more about identifying these illegal tactics, read Car Insurance Claim Denied? Here’s What to Do Next.

State-Specific Rules and Regulations

Insurance is regulated at the state level, meaning the rules governing claim denials, appeals, and legal remedies vary wildly depending on where you live.

California and Washington Insurance Laws

Both California and Washington operate under a pure comparative negligence system. This means you can still recover damages even if you were 99% at fault for an accident, though your payout will be reduced by your percentage of fault.

However, California has a strict “no pay-no-play” law. Under this rule, if you were driving uninsured at the time of the accident, you are legally barred from recovering non-economic damages (such as pain and suffering), even if the other driver was 100% at fault. Additionally, Section 533 of the California Insurance Code explicitly allows insurers to deny claims if the damage was caused by the willful or intentional misconduct of the insured.

If you are a driver in the Golden State, you can read more about your local rights in When an Insurance Company Denies Your Car Accident Claim in California, and make sure you are fully protected by comparing competitive rates for auto insurance quotes california.

Ohio and Louisiana Insurance Rules

Unlike no-fault states, Ohio and Louisiana operate under a traditional tort system. In these states, the driver who is determined to be at fault for the accident is financially responsible for all resulting medical bills and property damage.

In Ohio, the minimum legal limit for property damage liability is $25,000. If you are hit by a driver carrying only these state minimums, and your vehicle repairs exceed $25,000, their insurer will deny any payment above that cap. In Louisiana, you can escalate unresolved disputes by filing a formal complaint directly with the Louisiana Department of Insurance.

To understand your legal options in tort-based states, check out The Insurance Company Denied My Car Accident Claim. What Now?. If you have had your license suspended due to a prior uninsured accident or a DUI, you may need a specialized filing to get back on the road safely. You can read our guide on finding the cheapest sr22 insurance to secure affordable, state-compliant coverage.

Frequently Asked Questions About Claim Denials

Will appealing a denied claim increase my premium?

No. The simple act of filing an appeal or submitting a complaint to your state’s insurance commissioner will not directly increase your premium rates. However, if your appeal is successful and your insurer pays out a significant liability or collision claim, your claims history will be updated. This could affect your risk profile and lead to higher rates when your policy comes up for renewal. If you want to keep your costs as low as possible regardless of your claim history, check out our very cheap car insurance no deposit guide.

How many times can I appeal a car insurance claim denial?

The number of times you can appeal a denial depends on your specific insurance carrier’s internal policies and your state’s regulations. Most insurance companies allow for at least one or two rounds of formal internal review. If you exhaust your carrier’s internal appeals process, your next step is to escalate the dispute externally by filing a complaint with your state insurance commissioner or pursuing legal action. For more information on navigating these limits, see How to Appeal a Denied Auto Insurance Claim.

What happens if the at-fault driveru2019s insurance denies the claim?

If the at-fault driver’s insurance company denies your third-party claim, you have two primary options:

- File under your own policy: If you carry collision coverage or uninsured/underinsured motorist (UM/UIM) coverage, you can file the claim with your own insurer. They will pay for your repairs and medical bills (minus your deductible) and then pursue the other driver’s insurance company for reimbursement through a legal process called subrogation.

- File a lawsuit: You can file a personal injury lawsuit directly against the at-fault driver in civil court to recover your damages.

Conclusion

At Content Vibee, we believe that personal finance and insurance do not have to be overwhelming. Navigating an auto insurance claim denied letter is undoubtedly stressful, but with proactive planning, organized evidence, and a clear understanding of your legal rights, you can successfully challenge unfair decisions and protect your hard-earned money.

Whether you are looking for the best auto insurance quotes nc or simply trying to master your personal finances, we are here to help. Explore more personal finance and insurance guides on Content Vibee to find practical, actionable tips to keep your money safe and your future secure.